When Batteries Eat Themselves: What California Teaches Europe (and Spain, in particular) About Grid-Scale Storage

A forward-looking stress test for the Spanish grid — and the rest of Europe's battery build-out

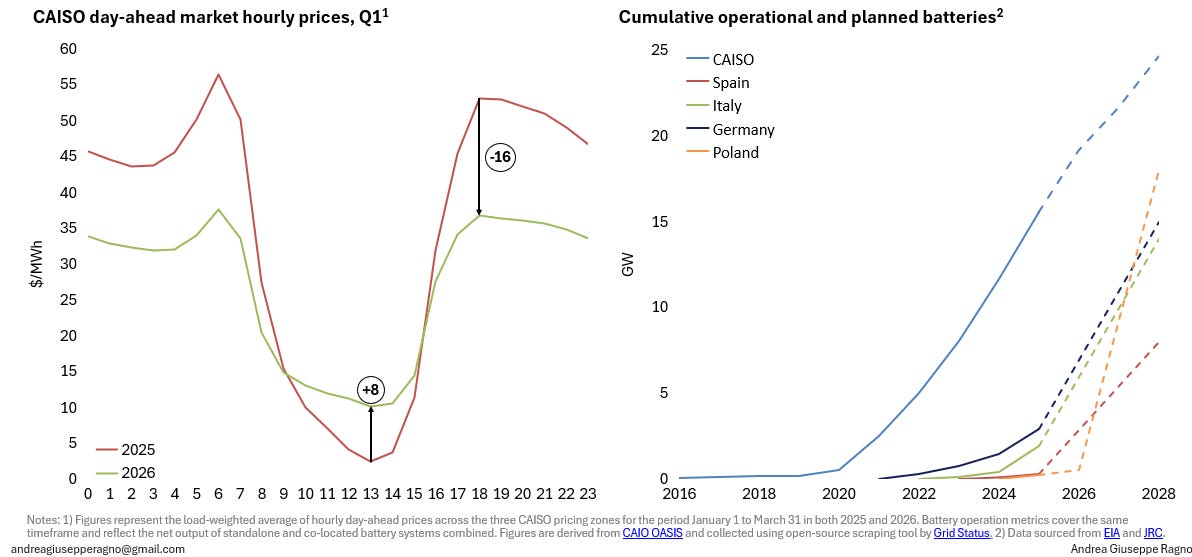

California’s electricity market, CAISO, seems to be the world’s most advanced laboratory for what happens when you deploy solar and battery storage at scale, fast. Between 2021 and 2025, CAISO’s battery fleet increased nearly six times — from 2.5 GW to 15.6 GW — compressing margins in ways that surprised even optimistic investors. Even if solar scaled fast, the evening ramp softened, and ancillary service prices collapsed under the weight of too much competing capacity.

Spain is about to run the same experiment. The two markets are more alike than most comparisons acknowledge. Spain’s peak hourly demand sits at around 40-44 GW — comparable to CAISO’s typical winter and spring peaks in the 38–46 GW range. On the solar side, Spain now has over 32 GW of installed PV capacity, recently surpassing wind to become its largest generation technology — a milestone CAISO crossed several years ago, where solar peaked at nearly 20 GW of output in 2024. The grid shapes, the solar ramp profiles, the evening demand curves — they rhyme closely enough that CAISO’s trajectory is less an analogy and more a preview.

Yet today, Spain has only around 300 MW of operational grid-scale battery capacity, against a permitted pipeline of nearly 40 GW across TSO and DSO connections already in processing. The PNIEC 2030 target calls for 22.5 GW of installed storage — roughly the scale CAISO reached by 2025–2026. The trajectory is nearly identical. The economics lesson has already been written. Europe just hasn’t read it yet.

The Arbitrage Squeeze in CAISO

The core promise of grid-scale batteries is energy arbitrage: charge cheap during the mid-day solar glut, discharge expensive during the evening ramp. In CAISO, this worked well across the years.

Two simultaneous forces drove this:

From the top: Evening peak prices simply stopped being very high. In 2022, only 14% of peak-hour prices cleared at or below $70/MWh — by 2023 that had risen to 39%, by 2024 to 86%, and by 2025 the figure stood at 97%. In 2025 specifically, better hydro conditions and cheap natural gas steadily ate into the marginal cost of evening generation, quietly eroding the price spikes that battery investors had counted on. That gas tailwind may not last — natural gas prices have since increased — but the structural shift in price formation is already baked in. The big paydays didn't disappear overnight; they faded year by year.

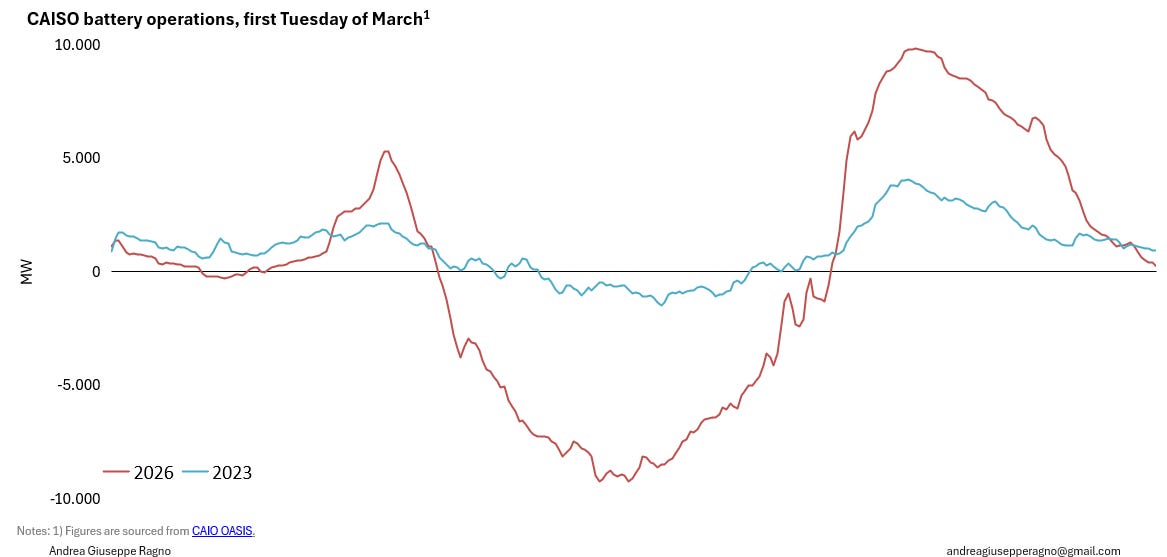

From the bottom: Batteries started undermining their own cheapest charging hours. As the fleet scaled, the collective mid-day charging demand grew from under half a GW in 2022 to more than 5 GW by 2025. Without that charging load, mid-day prices would have been far lower. Instead, batteries are effectively bidding against each other to charge, inflating the very floor they need to buy from.

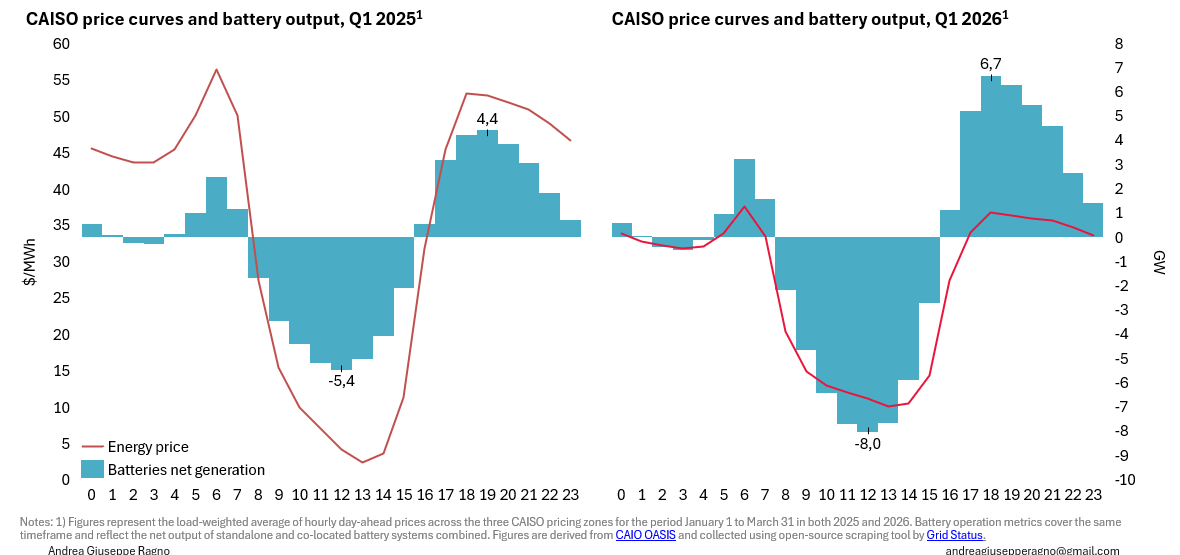

In 2026, this dynamic is already deepening and plainly visible in the data. The chart below compares CAISO’s average daily price curve and battery output profile across Q1 2025 and Q1 2026. In Q1 2025, batteries were pulling around 5.4 GW from the grid at mid-day and pushing back about 4.4 GW in the evening. One year later, those numbers have grown to 8.0 GW of mid-day charging and 6.7 GW of evening discharge — a 50% jump, in a single year. The price curve tells the same story: the mid-day trough is flatter and the evening peak is lower, with less than $30/MWh separating the two in Q1 2026. The spread that once made battery arbitrage so attractive has effectively collapsed to noise.

The dynamic is almost elegant in its logic. A single battery capturing the duck curve is a highly profitable asset. Thousands of batteries all chasing the same duck is simply a maturing market — one that rewards those who arrived early and forces later entrants to compete harder for thinner margins.

Ancillary Services: The First Market to Saturate

Before wholesale energy margins compressed, ancillary services — particularly Regulation Down (RD) and Regulation Up (RU) — were the primary profit engine for batteries. Batteries are technically ideal for regulation services: they respond in milliseconds, have no fuel cost, and can toggle direction instantly.

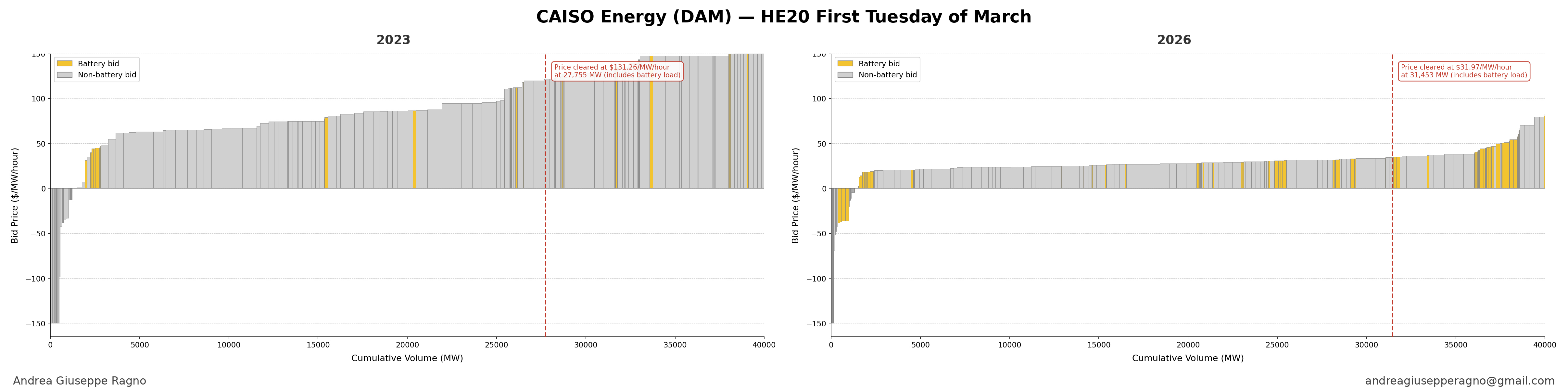

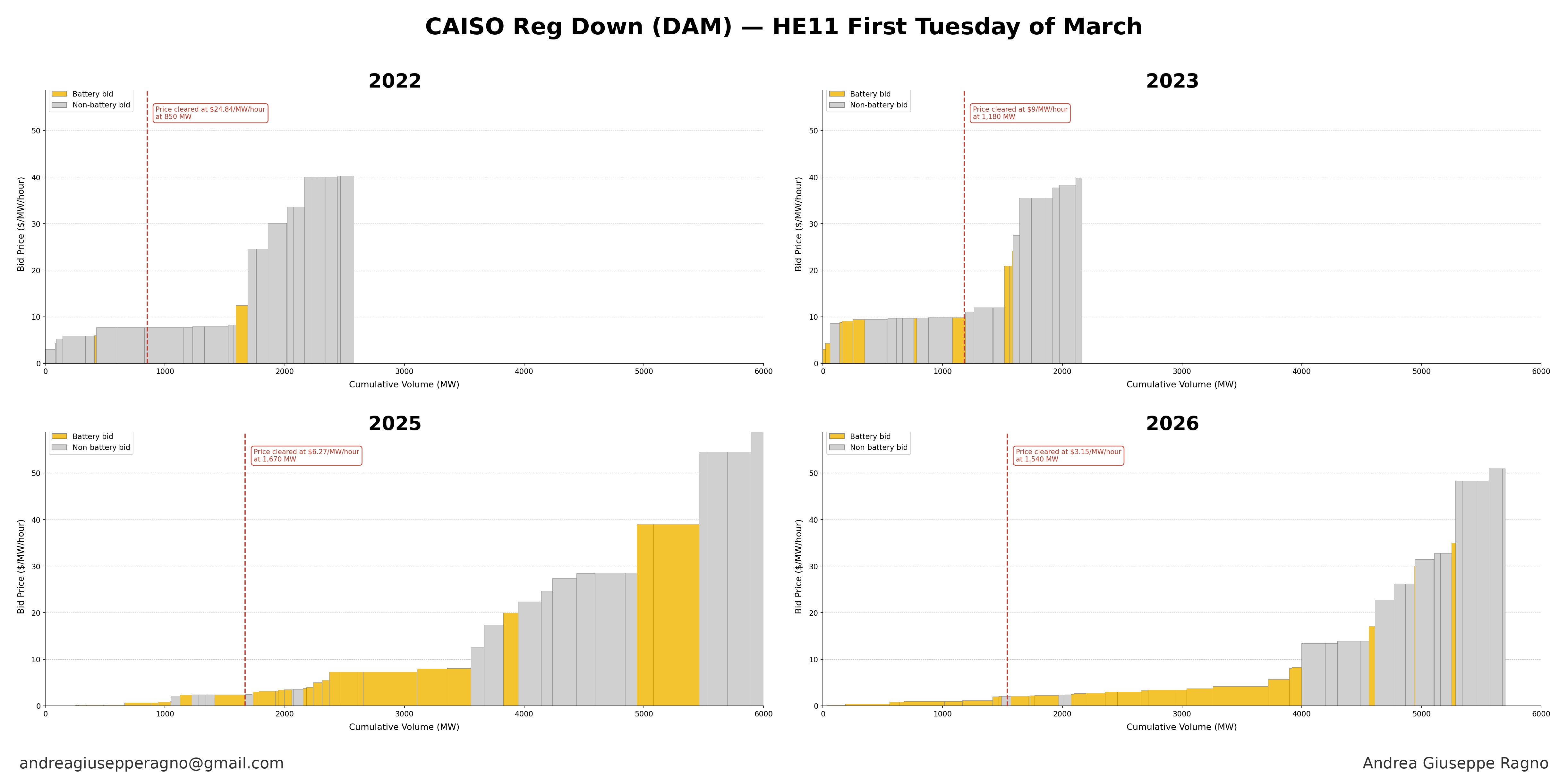

Look at the RD charts below. In 2022, battery participation was limited: a handful of bids clustered near the clearing point, with non-battery resources still filling most of the supply stack and setting the marginal price at around $25/MW/hour for 850 MW of procurement. By 2023, batteries had grown visibly in the stack but the clearing price had already nearly halved to $9/MW/hour. Fast forward to 2025 and 2026, and the picture is almost unrecognisable: the supply curve is dominated by batteries stretching far beyond the clearing point, and the price has collapsed to $6/MW/hour in 2025 and $3/MW/hour in 2026 — an almost 90% decline from 2022 in just four years.

Part of this is simply more batteries competing for the same slice of the market. But the choice of hour matters too. HE11 — the 10–11am window — sits right at the start of the solar ramp-up, and the solar resource itself has grown dramatically. In early March 2022, solar peak output across CAISO was just above 10 GW on a good day (e.g. on the first Tuesday of March); by early March 2026, it was approaching 20 GW, with wind adding another 2 GW on top. More solar flooding the grid in the morning hours means more downward pressure on prices precisely when batteries are trying to charge — and more excess generation that batteries are available to absorb. The RD market in HE11 is not just crowded with more batteries; it is operating in a fundamentally different grid environment than it was four years ago. Both forces point in the same direction: lower prices, thinner margins, and a market that has structurally repriced.

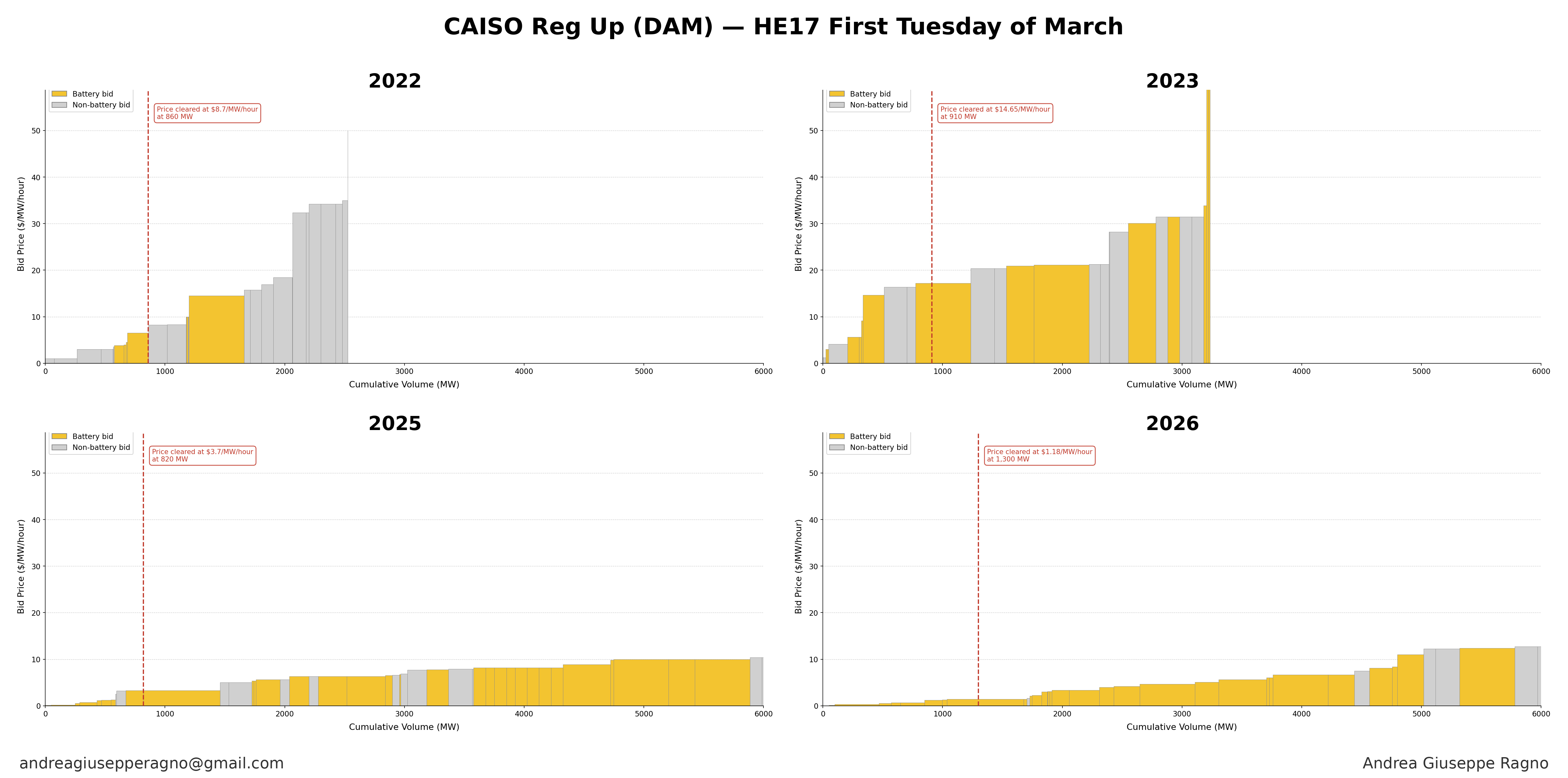

The RU charts tell the same story, though with a slight twist. In 2022, clearing sat at around $9/MW/hour at 860 MW — a relatively thin market, with batteries playing only a supporting role. By 2023, a surge in battery participation briefly pushed clearing volume to 910 MW while prices actually rose to almost $15/MW/hour, as the market absorbed new capacity without yet fully saturating. It looked, for a moment, like a healthy growth story. But the correction came fast: by 2025, prices had dropped to almost $4/MW/hour, and by 2026 to just $1/MW/hour — barely above zero.

Again, the hour matters. HE17 — the 5–6pm window — sits right at the start of the evening ramp-down, the moment when solar generation begins its steep daily decline and the grid needs resources ready to increase output quickly. In 2022, that ramp was modest relative to the resource stack. By 2026, the daily solar cliff is far steeper which means the evening ramp is larger, faster, and more predictable than ever. Batteries are perfectly suited to cover it, and they know it, and so does everyone else. What is most striking in the 2025 and 2026 panels is how the supply curve flattens almost entirely at near-zero prices across thousands of megawatts of battery capacity, with non-battery resources barely visible. The RU market has been fully taken over by batteries — and in doing so, largely hollowed out. When everyone shows up for the same trade, the trade stops paying.

Across both products, clearing rates deteriorated in parallel: batteries saw clearing rates fall at 4% per year for RD and 5% per year for RU, meaning not only are they earning less per MW cleared, but fewer of their bids succeed at all. Some batteries responded strategically, bidding 2–3x above the marginal clearing price to avoid being committed into ancillary services altogether — preserving capacity for energy market price spikes instead. Rational individually, but collectively it signals that the market’s own participants have started pricing in its limits.

Lessons for Europe — Especially Spain

The CAISO story is not a cautionary tale against batteries. It is a market timing and market design story. Here are the structural lessons that transfer directly to Spain — and to Europe more broadly:

The AS market saturates first, and fast. Spain’s regulation market today looks like CAISO’s in 2021 — thin battery participation, high clearing prices, strong revenues for early movers. The window of AS outperformance is real, but it closes quickly once more than a couple of GW of battery capacity enters the market. Spain is currently at under 300 MW operational; the pipeline means this window could close by 2030.

Zero-price hours are a leading indicator, not just an annoyance. Spain’s day-ahead market already saw hourly spreads increase 25% between 2024 and 2025, driven by growing solar curtailment and zero-price events. This is the attractive entry signal — it looks like CAISO in 2021–2022. But CAISO’s experience shows that batteries responding to those spreads at scale are the mechanism that compresses those spreads. The more batteries that enter to capture the opportunity, the less of it remains.

Market design matters more than capacity volume. CAISO’s margins eroded partly because of structural features: no capacity market premium for storage, limited scarcity pricing triggers, and a day-ahead market that rewards volume over optionality. European markets differ — Spain’s OMIE, MIBEL’s balancing services, and the European TERRE, MARI balancing platforms, and the capacity market recently approved by the European Commission all create different incentive structures. Spain in particular could benefit from designing AS procurement rules that avoid over-saturation by limiting the share any single technology can supply, or by creating longer-duration contract structures that reward duration over pure response speed.

The pipeline overhang is already here. Spain has 40 GW of battery storage in the permit pipeline against under 300 MW operational. Even if only a fraction of this materializes by 2030, the ancillary service market will reprice rapidly. Developers underwriting projects today against current market clearing prices are pricing in a market structure that won’t exist when their assets commission.

The CAISO lesson is ultimately this: batteries are not a scarce resource competing against gas turbines for a thin slice of AS revenue. They act as a commodity. And like all commodities, when enough of them arrive at the same time chasing the same price signal, the price signal disappears. Spain is standing exactly where California stood three years ago. The question is whether European investors, regulators, and developers will build the market design — and the portfolio strategy — that captures the window before it closes.

If you're looking to make a lot of money in the short term, then the article makes sense.

But if you see electricity as a common good, wuth the goal being an ability to reliably supply electricity to meet the demand, then the article is meaningless.

And that's why China will continue to accelerate away from the US in everything but inequality.

Treating essential services as a common good pays for itself in social cohesion, and more opportunities for more people.

Excellent article; congratulations. In the case of Spain, what essential precautions should be taken before desperately launching this battery capacity market? Should the state have its own battery infrastructure in the grid to, via the TSO, encourage optimal battery deployment?